"From Admitting Chinese Capital to Strengthening Digital Alliances" EU Faces a Strategic Crossroads Amid Decoupling From the U.S. and the Push for Technological Sovereignty

Authored On

Modified

Can Chinese capital provide a solution as the EU runs into funding constraints amid its decoupling-from-America trajectory? China’s Belt and Road strategy, which swept across developing nations, has highlighted the risks of debt-trap diplomacy Cooperation with Western allies and targeting strategic supply-chain bottlenecks emerge as alternative pathways

Calls are growing that the European Union (EU) should accept Chinese capital to secure the survival of its advanced technology sectors. As the risks associated with U.S. technology controls continue to mount, advocates argue that Europe must open its markets to China to secure growth financing and achieve technological self-sufficiency. Many experts, however, contend that such a scenario lacks practical viability, given that the dangers associated with Chinese capital have already been clearly demonstrated through initiatives such as the Belt and Road strategy.

Warning Signals Across Europe’s Advanced Industries

According to the South China Morning Post (SCMP) on June 17, Christian Noyer, founding vice president of the European Central Bank (ECB) and former governor of the Bank of France, said during an interview while visiting Hong Kong that “Europe must maintain an open attitude toward Chinese capital if it is to achieve genuine economic independence.” He added, “At a time when Europe urgently needs to develop its own AI ecosystem and advanced technology infrastructure, we can no longer rely exclusively on the United States.” Noyer further remarked, “No one knows when Washington may decide to restrict exports of critical products or complicate access to key foundational technologies,” warning that “unless Europe builds its own technological defenses, it will remain vulnerable to shifts in U.S. policy.”

His remarks directly address the predicament currently facing the EU. Europe is grappling with severe funding pressures across strategic future industries including artificial intelligence, clean energy, and defense. According to the competitiveness report submitted to the EU by former ECB President Mario Draghi, Europe must mobilize an additional $860 billion to $917 billion annually to catch up with the United States and China. In particular, simultaneously advancing digital transformation, decarbonization, and defense modernization will require not only fiscal expansion but also deeper capital-market integration and a redesign of industrial policy. In a separate assessment, the ECB estimated that public funding requirements for the green transition, digital transformation, and defense sectors approach $585 billion annually, while at least $121 billion of that amount remains unfunded each year under the current fiscal framework.

The challenge is compounded by the growing risks associated with U.S. technology controls. Since taking office, the second Trump administration has expanded regulatory scrutiny beyond mainland Chinese companies to include overseas subsidiaries with Chinese ownership. Washington has also begun treating access to certain AI models from key firms such as Anthropic, along with advanced AI chips, as matters of national security. If Europe fails to establish its own advanced technology ecosystem, bottlenecks in strategic industries could increasingly depend on U.S. approval rather than market competition. This concern underpins Noyer’s argument for maintaining openness toward Chinese capital. Excluding China entirely could leave Europe unable to secure sufficient investment resources, increasing the risk of strategic isolation in global competition. Conversely, selectively utilizing Chinese capital under strict security reviews and regulatory safeguards could reduce dependence on the United States while accelerating the development of Europe’s own AI and advanced technology infrastructure.

The Core Risks Embedded in Chinese Capital

Many experts nevertheless argue that increasing dependence on Chinese capital represents an excessively risky choice. China’s Belt and Road Initiative (BRI), its flagship overseas infrastructure investment strategy, has previously increased debt burdens and sovereignty risks in several emerging economies. First proposed by Chinese President Xi Jinping in 2013, the initiative envisions the creation of a land-based Silk Road Economic Belt linking China with Central Asia, the Middle East, and Europe, alongside a 21st Century Maritime Silk Road connecting Southeast Asia, the Indian Ocean, Africa, and Europe. While officially presented as an effort to strengthen growth foundations in developing countries through infrastructure investment, the initiative ultimately evolved into a form of debt-trap diplomacy, with Chinese state-owned banks and enterprises dominating financing and construction while increasing recipient nations’ dependence on Chinese debt.

Sri Lanka is widely cited as a leading example. The country relied on Chinese financing to build the Hambantota Port in its southern region, but the project failed to generate the expected revenues, leading to mounting repayment pressures. In 2017, the Sri Lankan government signed an agreement granting China Merchants Port Holdings a 99-year lease on the port’s operations. The transaction was valued at $1.12 billion. Laos has similarly become a prominent example of both the benefits and drawbacks of the Belt and Road Initiative. The country significantly expanded borrowing to finance major infrastructure projects, including a railway linking Laos and China, hydropower facilities, and power-transmission networks. Repayment pressures intensified before those projects could generate substantial returns. Today, Laos faces a severe economic strain marked by heavy external debt, high inflation, and currency weakness, placing essential spending on healthcare, education, and climate resilience at risk.

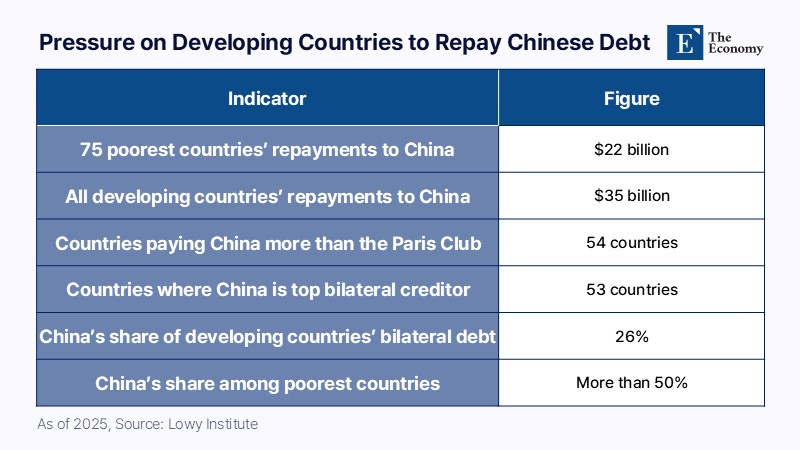

Numerous other developing nations are also struggling under Chinese debt burdens. According to Australia’s Lowy Institute, debt-service payments owed to China by the world’s 75 poorest and most vulnerable countries reached nearly $22 billion last year. Across all developing nations, the figure rises to approximately $35 billion. Among 120 developing countries, 54 owed more in repayments to China than to all Paris Club creditors combined, while China had become the largest bilateral creditor in 53 countries. As infrastructure loans issued during the early stages of the Belt and Road Initiative mature, China’s role has shifted from provider of new development financing to debt collector. These developments illustrate that Chinese capital can function as a double-edged sword, creating risks related to long-term policy dependence and control over strategic assets rather than serving solely as an investment resource.

Alternatives to Support Europe’s Post-America Strategy

Expanding cooperation with Western allies is widely viewed as an alternative path for mitigating these risks. The EU has already established digital partnerships with countries closely aligned with the U.S.-led security and technology order, including South Korea, Japan, and Canada.

Japan was the first partner to formalize such cooperation. The EU and Japan launched their first Digital Partnership during the EU-Japan Summit in May 2022, and cooperation has since expanded to encompass AI, data governance, quantum technologies, semiconductors, digital infrastructure, and online platform regulation. During the fourth EU-Japan Digital Partnership Council meeting held in Brussels last month, discussions focused on deepening regulatory, research, and industrial cooperation in AI, data, quantum technologies, and semiconductors.

Canada launched its Digital Partnership with the EU in November 2023. Areas of cooperation include AI, quantum technologies, semiconductors, cybersecurity, online platforms, digital identity, and secure connectivity networks. At the inaugural EU-Canada Digital Partnership Council meeting held in Montreal in December last year, key topics included AI cooperation, digital identity wallets, trust services, independent media, semiconductor supply chains, and cloud and data-center infrastructure. South Korea signed its Digital Partnership with the EU in November 2022 and, on June 10, signed a separate Digital Trade Agreement during the EU–South Korea Summit in Brussels. Designed to complement the EU–South Korea Free Trade Agreement that entered into force in 2011, the accord establishes detailed rules governing cross-border data flows, electronic contracts, electronic signatures, consumer protection, and online commerce.

Another viable path toward technological self-reliance is developing unrivaled competitiveness in strategic supply-chain bottlenecks. The Middle East offers a compelling example of the effectiveness of this approach. For decades, Gulf energy producers have exercised substantial influence over global energy markets through their oil and natural gas resources. More recently, that influence has begun extending into AI infrastructure. In May last year, the United Arab Emirates (UAE) and the United States agreed, during President Trump’s Middle East tour, to develop a 5-gigawatt AI campus in Abu Dhabi. According to UAE officials, the project will become the largest AI infrastructure hub outside the United States, enabling American hyperscalers and major corporations to utilize regional computing resources. Subsequently, G42, OpenAI, Oracle, Nvidia, SoftBank, and Cisco announced plans to build a 1-gigawatt “Stargate UAE” computing cluster within the campus. Around the same period, Humain, an AI company backed by Saudi Arabia’s sovereign wealth fund, announced plans to construct an AI factory with up to 500 megawatts of capacity in partnership with Nvidia.

Middle Eastern countries are attracting attention in the AI infrastructure race largely because of their abundant and inexpensive energy resources. Electricity prices in Saudi Arabia range from approximately $0.02 to $0.05 per kilowatt-hour, substantially below levels in North America and Europe. This provides a direct cost advantage for operators of large-scale AI computing facilities. The region’s geographic position is equally significant. Situated at the crossroads of Europe, Asia, and Africa, the Middle East serves as a strategic hub capable of targeting multiple Global South markets simultaneously. Rapid decision-making processes further enhance its appeal. Saudi Arabia and the UAE combine sovereign wealth funds, state-owned enterprises, and government-led industrial strategies to execute large-scale infrastructure projects at remarkable speed. Unlike the United States and Europe, where coordination among private companies, local governments, and utility providers often delays projects, these countries can rapidly concentrate capital and administrative resources following strategic decisions by national leadership. Rather than focusing on developing high-performance AI models themselves, they are exerting influence within global technology supply chains by providing the foundational infrastructure upon which the AI industry depends. It is a clear demonstration that industrial dominance can emerge from control of critical infrastructure as much as from leadership in finished technologies.

Similar Post