Why Europe Is Falling Behind in the AI Adoption Race

Published

1 The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

2 Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

The article argues that the widening AI adoption gap between the U.S. and Europe is not a matter of cultural excess, regulatory excess or digital underprovision. It reflects a more fundamental institutional divergence between economies that concentrate elite technical talent, abundant risk capital and governments willing to support AI deployment and economies where these elements are still fragmented across institutions. The U.S. lead reflects the capacity of firms, universities, financiers and public agencies to transform AI from an available technology into an organizational capability while China has built a state-led version of the same triad. Europe, by contrast, has excellent research centers and technological assets that are not sufficiently converted into adoption. Investment channels, digital skills, public support, and competitive pressure to innovate do not yet appear substantial enough to turn research strnegth into scaled deployment. By contrast, the case of Japan reveals a similar pattern of lack of organization and speed notwithstanding advanced technical capacity. The article concludes that global AI leadership will depend more on institutional capacity to generate learning, experiments and scaled change within organizations than on raw access to technology.

1. Introduction - AI Adoption Is an Institutional System, Not a Tool Gap

The usual historical account of the artificial-intelligence gap widening between the U.S. and Europe is now too superficial. It places too much importance on regulation, on culture, or on general worker enthusiasm, but these are downstream explanations of a more profound configuration of power. The countries advancing most rapidly in AI are not merely those with superior software, nor those more welcoming to new modes of experimentation.[1] They are the countries actually achieving the following three things at scale and in combination: a networked cluster of leading quantitative minds, abnormally deep pools of risk-hungry capital and a state apparatus willing and able to fund research, expand compute and data infrastructure, use procurement strategically and support diffusion. The U.S. has by now assembled all of these components most completely, but China, a different style of political economy, has assembled a version of the same triad and so remains a systemic competitor. Europe, meanwhile, has components of each, but not assembled as a system. Hence, the growing transatlantic divide despite the fact that Europe has many fine universities, strong research institutes, innovative corporations and a well-functioning regulatory authority.

Recent comparative evidence clearly takes the divergence beyond 'anecdotal': in early 2026, 43.0% of U.S. employees used AI in the workplace, relative to an average of 32% across six European countries surveyed[2] (it was 25.6% in Italy and 36.3% in the U.K.); and when intensities, rather than incidences, are examined the difference is even starker: 5.2% of all U.S. work hours were spent using AI, about twice as much as in the U.K., Sweden and the Netherlands and over three times as much as in Germany, France and Italy.[3] And differences at the firm level are just as sharp: in the 2025 Eurostat enterprise survey, about 20% of firms in 32 European countries used at least one AI technology in 2025, with adoption levels above 35% in Nordic frontrunners and falling below 10% in several southern and eastern laggards;[4] European productivity evidence abounds: since 2022, U.S. industries with a 10 percentage point higher worker AI share exhibited 2.9 additional percentage point aggregate productivity growth over the pre-pandemic trend, consistent with similar European findings.[5]

Yet the most interesting discovery from the recent Brookings CEPR and St. Louis Fed analysis is not just that the U.S. leads. It is why. Demographics, industry makeup, education and the size of the average firm partially, but not entirely, determine the U.S./Europe standoff. After these structural factors are controlled for, management and institutional push factors explain much of the gap: workers learn to use AI more quickly when companies actively push adoption, invest in the right organizational structure and build systems to facilitate the AI. Once employer encouragement and workplace support are included, over four-fifths of the U.S. excess of adoption over Europe can still be explained.[6] That conclusion matters because it establishes that AI appears no more like a consumer good than as a general-purpose systemic technology with returns that hinge on deliberate managerial response, organization-changing reconfiguration and post hoc complementary investment. U.S. firms, then, don't just get access to better tools than Europeans; they are too willing to harness talent, money and organizational aspiration to those tools.[7]

This is also why implying AI as an unsophisticated tool for improving productivity is incorrect. The first-order improvements are already definite. In the customer-support system trial by Brynjolfsson et al., a generative-AI-assistant was able to increase productivity by roughly 14%, exhibiting positive effects particularly for new and less adept employees.[8] Causal evidence from European firms points in the same direction: AI implementation increased working productivity by around 4% in the short-term period without immediate job reduction, with bigger gains observed most intently in medium/large firms occupying AI alongside software, data and human workforce training.[9] Nevertheless, these results represent a second-order mode of innovation, not a prognosis. Productivity gains appear where institutions can finance intangible assets, reorganize work and embed AI into operational routines. Where workers are not able to work with an AI intermediary, AI will present itself in a reduced state: incremental, superficially integrated, often relying on foreign technological networks. Consequently, the political dilemma is not who has access to AI tools, but who can build the institutional structure that turns AI access into a cumulative advantage.

This helps explain why China shows up where it does. The U.S. remains the undisputed leader in frontier private AI investment and significant model output. In 2024, private AI investment in the U.S. stood at $109.1 billion, 11.7 times higher than China’s $9.3 billion and US-based institutions produced 40 significant AI models compared to 15 from China or 3 from Europe.[10] Yet China still holds the world lead in AI patents and remains formidable in terms of Chinese leadership in publications, industrial robotics, semiconductor-led industrial policy and state-sponsored funding.[11] In March 2025, Beijing announced a national venture-capital guidance fund expected to marshal around 1 trillion yuan for technology start-ups, especially in AI and long-standing industrial policy still continues to subsidize strategic zones, compute, land, credit and commercialization corridors.[12] China is not beating the U.S. on every frontier metric. This matters because it has mustered enough brains, capital and state capacity to stay seriously competitive in the AI race. Europe's weakness is more structural: it might have one of the three components at once, but almost never all three together.

If a contest for the most accurate prediction is in order, fairness might dictate recognizing the strongest rival. Certain firm-level surveys do not seem to notice much difference. In the 2025 EIB Investment Survey, 37% of firms in the EU indicated generative AI use, versus 36% of firms in the US.[13] Such a result-the closest margin in the broadest metrics-appears not to resurrect the argument for a large disparity. When considering other dimensions of adoption, such as the scope of use within a firm, the United States performs better in that survey as well: 81% of AI-adopting U.S. firms, as opposed to 55% of sharing firms in the EU, employ AI in more than two activities.[14] And, when studying the relative importance of survey focus, the St. Louis Fed has demonstrated that how a survey is worded can make all the difference. U.S. surveys, which narrowly assess AI use in producing goods and services, nearly doubled when asking broader questions regarding several AI technologies for every business purpose.[15] The takeaway is not that Europe is just as far along. Rather, the breadth of revealed exposure and the change in the scale of integrated operational AI use are different issues altogether. Europe is not a place of AI abandonment; on the contrary, it is a place of a weaker intensity, weaker scaling and weaker institutional complementarities.

2. Why Europe Converts AI Access Into Slow Adoption

The first drag on Europe is investment and this is the least ambiguous part of the story. Europe is still institutionally and demand-side inherently weaker than the United States in turning savings into technological innovation at scale. Stanford's 2025 AI Index recorded $109.1bn of private AI investment in the U.S. In 2024, China was at $9.3bn and the U.K. At $4.5bn, while Europe's frontier-model output remained limited, with only three notable models.[16] Draghi's competitiveness review identified the deeper background: Europe was "stuck in a static industrial structure" and without an EU company above 100 billion in market value built from scratch in the last fifty years, whereas all six American companies built between 1.0 trillion and 2.0 trillion in market value in the same period.[17] It also found that in 2021, EU companies spent about half as much on research and innovation as a share of GDP as U.S. companies.[18] IMF analysis confirms the firm-level aspect: Venture-capital investment in the EU has been less than 0.2% of GDP over the last ten years, compared with nearly 0.7% in the U.S., while small-scale markets and limited market-oriented financing hamper Europe's frontier firms.[19] Indeed, Europe's own institutions recognize the scale-up gap: EIB studies conclude that EU-scale-ups attract only about half the capital as peers in Silicon Valley.[20] AI, which requires massive spending on compute, skills and business, penalizes that disparity more severely than the previous waves of innovation in software.

The second drag is much more discreetly described as “poor education". Educated citizenship is not Europe's issue in any civilizational sense. Indeed, Draghi's very first mention of Europe's more-than-adequate education systems was in the context of how great they are. The problem is translational: Europe is under-producing, under-retaining and under-redeploying sufficient human capital relevant to the technology fast enough. Eurostat reported that only 56% of EU citizens ages 16-74 had at least basic digital skills in 2023; the EU missed its 2030 Digital Decade target by 24 percentage points.[21] In 2024, the EU had 10.3 million ICT specialists- almost 9.7 million shy of its 2030 target-and in 2025, these specialists accounted for 5% of employment, with stark variation across member states from 8.9% of employment in Sweden to 2.5% in Greece.[22] The Commission's own Union of Skills program admits the gravity of this shortfall: Almost four out of five SMEs find it difficult to find the right talent while one out of four 15-year-olds falls short in reading, mathematics and science.[23] And this is not just a coding problem. It is a pipeline problem, from quantitative foundation to advanced technical training to labor-market matching.

The talent problem is exacerbated by retention and mobility. Europe clearly trains capable researchers and the Commission’s AI Continent webpage accurately characterizes the Union as having “unmatched talent". However, evidence on talent flow over the last few years suggests that European countries are losing a huge number of these world-class national and international AI talent to the United States, while relocations of the world's most innovative EU startup and scaleup companies cite easier access to capital, larger homogeneous markets, more comfortable business environments and more mature pools of commercial expertise as the main reasons for moving abroad.[24] Here is the familiar European pattern: instead of putting to good use the countries' strong research superstructure, the knowledge creation phase can be worldwide competitive, but the phase of commercialization and scale-up can only be outsourced. This is why Europe's weakness is systemic rather than intellectual: its universities and labs can still generate able people, but their institutions evidently cannot keep them within a significant superstructure in which frontier science, infrastructure, late-stage finance, product management and indeed market aggregates serve as inputs. The conclusion for European higher education and governance should not be to elicit Silicon Valley-like utopias of residential life. It should instead be to design stronger interfaces for top-of-the-line mathematics, computer sciences and engineering on the one hand and commercialization on the other, including mobility in the form of sharing tenureships and research infrastructure, digitized and in-person-based AI apprenticeships and non-captive professional career tracks that allow the industry's top talent to stay in the Union.

The third drag is government support, not because Europe has no policies but because its support has ever been fragile, under-tagged and if operational, erratic. OECD 2025 review of EU Coordinated Plan on AI found that less than half of EU member states had dedicated budgets for national AI strategies; public investment was often accreted into wider digitalisation envelopes, that made it hard to track it; monitoring and evaluation varied widely; only around one-quarter of member states had programmes for attracting and retaining AI postgraduate students and career reseachers and only one country had schemes to help non-academic organisastions recruit AI talent.[25] Similar findings are listed in the OECD review, which also pointed out that there was little trans-border coordination, that data-sharing remained ad hoc and the support for SMEs was fragmented. This may sound like an administrative detail, but it matters greatly in a market where scale, speed and complementarities rule; fragmented support adds transaction costs, delays procurement, hampers feedback on bet-like experimentation and makes deployment dependent on local champions rather than systemic design.

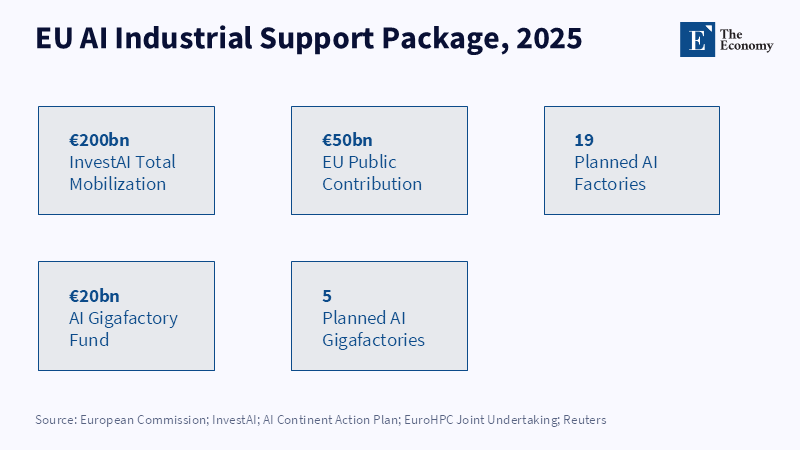

Europe has roused itself and it has to be said that a sober analysis must conclude that policy shifts significantly between 2025 and 2026. The AI Continent Action Plan now speaks in billions rather than millions: a 200 billion European shot to drive AI development, the possibility of five AI gigafactories and 19 smaller AI factories to create startups, industry and academe and a new confrontation with the need to create a real internal data market and train and hold onto the world’s best AI brains.[26] It has also launched an Apply AI strategy and extended its workforce initiatives through the new AI Skills Academy and the Union of Skills. None of these are trivial steps and they represent a long-overdue admission that Europe cannot regulate itself to global competitiveness. But they also point to the extent of Europe's shortfalls and the extent to which Europe is seeking to replicate an intelligent ecosystem built by the U.S. over its decades of research-focused universities, national labs, AI institutes, defense contracting, venture finance, procurement and immigration counterbalance. On the American side, the state has not been absent and has not simply gone purely deregulatory: the National AI Initiative ecosystem has green-lighted 25 AI Research Institutes, NSF contributed another $100M in 2025 for five additional institutes, the White House established an AI Education Task Force in 2025 and the 2025 AI Action Plan committed state funding for testbeds, assessment science, interpretability and sectoral application.[27] Europe continues to wake up, but it is still playing catch-up from a far weaker institutional starting point.

However, there is a deeper reason why these gaps matter. AI does not reward "half readiness". Quite the opposite: it accentuates existing asymmetries because it is highly complementary with intangibles-managerial talent, computing, organizing data and skilled workforces. The OECD's research on emerging divides shows that the diffusion accelerated in 2023-24, but mainly because leading profiles pulled ahead, not because laggards leveled up.[28] The most substantial upgrades took place in larger companies, capital regions and more knowledge-intensive services; at the same time, the gaps among regions, sectors and firm sizes grew.[29] Europe thus faces a twofold danger: chronic under-spending will mean falling behind the U.S. On the first front, uneven diffusion will generate a self-reinforcing internal hierarchy between Nordic and non-Nordic front-runners, between large businesses and SMEs and between core and peripheral economies. These are the moments where the educational and public sector challenges make themselves felt. Schools and universities will be under pressure to build greater quantitative, numerical and evaluative skills just at the time weak regional labor markets give weaker signals. Treating computational reasoning as an optional specialization rather than a necessary skill in school systems would deepen the territorial divide further. Meanwhile, public administration systems will require procurement, training and data management architecture that has to be distributed for staff and students without transforming State facilities into passive consumers of foreign formats. Skill training is no social add-on in the age of AI: skills are what turn diffusion into a sustainable trend.

A somewhat fair counter-argument is that Europe's style might have its benefits-greater protections, more rights, more consumer confidence and less reckless deployment. There is truth in that claim. Perhaps Europe won't have much of the waste, fraud, or social breakdown that accompanies booming technologies elsewhere. But the trade-offs are often misunderstood. It's not a choice of rapidity versus safety. It's a choice of regulatory regimes clinging to an economic-growth machine versus replacing one. Europe has been very good at setting rules, but lagged behind in beating the competition at building the markets, capital and human-capital institutions that give those rules their economic pulse. And that is why the core assertion endures. The US-Europe difference isn't due to any one factor-it's due to Europe's failure to anchor a self-reinforcing cycle between brainpower, financial motivation and institutional state aid.

3. Comparison to Japan: Similar Lag, Different Machinery

Japan's predicament invites such comparison because it can serve as an indication of what Europe's own house would look like should similar outcomes materialize under a different institutional temperament. The OECD 2025 evidence on use in the SME sector established funding-generative-AI as the lowest deployed use across all the examined countries – 23.5% as against 38.7% in Germany – as did the 2024 Reuters-Nikkei survey, which underlooked presence, planning and not undertaking AI implementations in Japanese companies – 24%, 35% and 41% respectively.[30] OECD's Economic Survey on Japan has been outspoken about the broad context underpinning such under-performance.[31] Business dynamism remains muted, start-ups are fairly infrequent, the exit of low productivity firms is lackluster and triple-digit guaranteed government loans patronized by banks have historically diminished incentives for a brisker transfer of credit.[32] In that sense, Japan models Europe less on its format than in its content: the reduction in diffusion roadblocks stems not from a lack of cognizance but from institutional conditions that insulate incumbents from pressures and whose repercussions for the delay are mild.

The parallel continues with human capital, though again the details are not exactly the same. Japan is not at all short on engineering strength in the abstract, but its most advanced human capacity has rather internal limits. The OECD has pointed out, inter alia, that the fraction of Japanese graduates in Science-, Technology- and Engineering-related fields is relatively low, especially for women, while data from Education at a Glance reveals that Japan has among the lowest rates in the OECD for female entrants into Science-, Technology-, Engineering- and Math-related master's and doctoral programs.[33] So it is not a matter of lacking technical competence in the domain of robotics, manufacturing engineering, or industrial process automation; Japan is extremely good at advanced industrial systems and applied industrial disciplines. But Japan has a smaller-than-it-seems working pool of frontier, interdisciplinary and mass-deployable AI human capital and that makes a difference because competition in that space is becoming more about statistics, software engineering, used-capacity processing resources and product logistics and countries with less deep supply chains in those areas can easily remain technically sophisticated while still becoming slow to diffuse AI.

The investment more generally reminds us of Europe's problems, but is managed according to a different internal logic. OECD 2026 work reiterates the weak dynamism of business as a trap to productivity, while Reuters reported that in Japan, policymakers are now seeking to cautiously allow more 'zombie' companies to close or merge as a means of restoring, what the officials call, economic metabolism.[34] While Europe's financing issue tends to be framed as fractured capital markets and inadequate financing for late-stage risks, Japan's looks more like "endless tolerance of incumbents, survivorship in the absence of renewal and belated reallocation". Such a structure is, of course, even less suited to AI. Frontier AI demand capital, technical services and organizational willingness to uncertain pay-offs, swift purchases, supplier churn and pilot failures. These are precisely the cumulative conditions where weak dynamism and preserved stability become prohibitively expensive.

There is, however, one area where Japan can have a more transparent catch-up route than Europe. Since 2024, the Japanese state has taken firm steps to establish an official system for AI development and use within the public sector. NEDO and METI introduced GENIAC to improve domestic foundation-model expertise through computing power provision, demonstration assistance and cooperative tools; the government then established an AI Act in 2025, adopted an AI Basic Plan and founded an AI Strategic Headquarters, led by the prime minister and comprising all cabinet ministers.[35] The plans of the Digital Agency for "GENAI" are particularly illuminating: in Fiscal Year 2026, 180,650 civil servants of every ministry and agency in the entire government are expected to be granted Generative-AI access, with the stated aim that the state should "set the example" and drive an AI-conversion of administrative practice.[36] This isn't a recipe for automatic prosperity, but the prospect of a credible chain of propagation from public commissioning and administration into the national corporate landscape. Japan, where an extensively collaborative bureaucratic implementation capacity has traditionally existed, could therefore translate this into an especially quick Follower response if public-sector leadership begins to diminish the implementation organizational costs.

This, then, is the real similarity and the real difference. Europe and Japan have both fallen behind the U.S. because they have failed to replicate that unique American integration of deep talent pools, aggressive capital investment and operational state intervention. Japan's falls are accentuated more starkly by organizational hierarchy, consensus-oriented decision processes and the glacial pace of reallocation in firms and credit industries. Europe's falls are accentuated more starkly by jurisdictional fragmentation, more fragile scale-up finance and a political legacy that grew more confident in rule-setting than in industrial coprocessing. It's possible that political pathways out are therefore different. Japan may improve through coordinated public leadership; Europe’s route is harder because it depends on market integration, capital-market reform and managerial renewal across many jurisdictions. Its reverse strategy must be enabled through the more arduous processes of market unification, infrastructure projects and human capital rebalancing. In effect, Japan resembles Europe more than it does the United States, but it does not resemble it completely. It resembles it in inertia; it diverges from it in the mechanics of how to surmount it.

4. Common Element Behind the Scenes: Low Competition and Protected Incumbency

The unexplained common denominator that seems to be missing between Europe and Japan is not solely "regulation" or "culture", taken separately. There is low competitive pressure on incumbent firms, which alleviates the pressure to innovate via workers retooling, technological upgrading, institutional innovation, or business model innovation. The empirical literature increasingly points in that direction. The NBER 2026 international firm survey established that AI is particularly prevalent in the younger, more efficient firms.[37] ECB research also indicates that the younger enterprises (which are bound to survive since existing ones do not) of the euro-area are, on average, three times more productive than the older ones and spend much more on software, databases and specialist services.[38] The logical consequence is the following: AI dissemination is inherently driven by firms that need to grow, expand presence, innovate and stay efficient; otherwise, "market structure", "finance," and "company organization" norms can slow down or halt the adoption process. The issue is not simply the availability of AI. It is rather the incentives to adopt it before your competitor.

In Europe, the foreclosure of "old firms" is mediated less by direct favoritism than by market fragmentation, administrative burdens, bank-based finance and high fixed cost barriers to cross-border expansion. Draghi's 2024 report illustrates it vividly-Europe suffers from a structural deficit of new companies capable of either shaking up incumbent industries or launching new growth engines.[39] This qualification feeds on itself. IMF analysis highlights small- to medium-sized domestic markets together with subordinate market-based finance as main barriers to the growth of frontier firms, while Draghi emphasizes institutional obstacles and legal constraints preventing corporate cross-border expansion within the Union.[40] Both findings resonate with the recent EIB and EC reports. Sixty-two percent of European firms complain about internal market fragmentation; regulation imposes a 2% loss of turnover on SMEs; and transnational reallocation of start-ups and scale-ups is driven by market size, better VC access, more supportive institutional framework and superior commercial talent.[41] In such an environment, the need to adopt challenging organizational configurations may be postponed by incumbent firms, while less disadvantaged entrants could quit the race to become dominant ordinary firms. That constitutes the entry barrier of low competition.

This also accounts for why the standard claim that Europe is merely 'over-regulated' is both true in part and incomplete in form. Europe regulates large foreign digital firms in a very aggressive way; the Commission has filed a DMA against Apple and Meta, showing that Brussels is prepared to sanction incumbent platforms before they have gained a dominant position.[42] But penalizing the gang of very large platforms is a very different task than producing the local challengers. In the contestability equation, we need not only penalties for entrenched firms, but also other institutions that encourage candidate entry -- integrated capital markets, harmonized corporate law, quick licensing and procurement proceedings that can be won by young firms and regulation burden whose compliance burdens do not weigh more on digital scale-ups. Europe has been much more effective on the ex post and rule-setting side than on the production of champions side. The core issue, accordingly, is not that the Commission acts against U.S. Firms, but that Europe has too often resorted to regulatory sovereignty as an Ersatz for technological sovereignty. AI makes that substitution painfully transparent.

Japan's version of low competition is more cultural and credit- mediated than jurisdictional. OECD's 2024 and 2026 reports document a corporate environment with weak movements of entrants and exiters, a long-run support of low-productivity SMEs and sluggish flows of resource reallocation.[43] Under certain conditions, the costs of switching suppliers or other inputs, reorganizing tasks inside firms, or taking tough decisions with respect to the procurement choice are not fully paid at the bidding occasion in competition, but through hierarchy, permanence rules and holding consensus. The public records are certainly more cautious than the colloquium, which a practitioner often invites to write down a textbook analysis. Yet the general trend is clear. Among Japanese workers and firms, the AI adoption rates are comparatively low, while the government's official report admits Japan's need for a stronger pace of business dynamism, firmer support for start-ups and a more solid culture of innovating to win market share.[44] When managers anticipate no immediate chance of being severely financially sanctioned for the postponement of AI implementations and no internal benefit for taking AI-inducing technological risks, then it is easier to delay AI. Thus, Japan can be perched on its technological prestige in the fields, yet still constrained by its conservative organization at the level of business firms.

The second-order effects are worse than what the adoption figures show. In low-competition settings, adoption is not only slower, but it also changes human capital formation and the distribution of future rents. Delaying adoption also means delaying demand for new skills. Universities, vocational systems and schools respond rationally to those weak signals by maintaining older curricula, weaker ties to industries and less CPU upgrading. As time goes by, this effect will only be amplified. Europe already has digital-skills deficits and a shortage of ICT specialists. Japan's thinner pipeline of AI talent is further hindered by weak STEM participation among women. Not only this, but the firms that do adopt are not the average business. Causal European evidence suggests that most of the productivity benefit goes to medium to large firms, for whom the effect is strongest when accompanied by complementary investments in software, data and training.[45] OECD evidence suggests that early AI adopters are widening the gaps between places, sectors and firm sizes.[46] We are witnessing a familiar but newly intensified pattern: winners build up, losers catch up and divergence increases across regions, firms and workers. To call AI a neutral efficiency device is to ignore its role in sorting.

The diagnoses have concrete implications. For educators, the focus should not be simply on imposing classroom automation for every subject but on ensuring stronger fundamentals in mathematics, statistics, computer science, model validation and translation with embedded apprenticeship-like connections between high-intensity research and high-intensity deployment. AI should be taught as a system requiring judgment, data management and expertise in an area, not as a knowledge bank replacing them. For firms, governance must graduate from "AI policy" to purchasing criteria, endorsed use-cases, employee preparation and research collaborations that enhance institutional capacity rather than merely monitor wrongdoing. For states, the strategy must be still more aggressive: augment late-stage risk capital; break down regulatory barriers across nations; broaden skilled migration pathways; maintain a compute and data advantage; exploit the state's buying power for lead markets; and account for adoption in a way that recognizes deep operations, not just broad reach.[47] None of these measures is politically simple. All are vital. The world's most competitive AI economies over the next ten years will not be the ones that promise disruption the most. They will be the ones who drive the interaction of competition, capital, talent and executive capacity to compel fast organizational learning.

The upshot, then, is far more emphatic at the conclusion than at the outset. The U.S. is surging ahead in AI adoption compared to Europe, not because Americans are more inherently excited about new software or because Europeans are somehow naturally built to innovate less; the difference is institutional. American society combines elite quantitative talent with incredible levels of private-sector investment, along with a government that has at least kept investing in science, funded research, continuing to build labs, designing procurement and training workforces at scale despite the ideological seesaws. China has built a more centralized version of the same three-part system, making it a credible challenger even where it still trails the United States. Europe has some of these technologies, but not at scale, i.e., with a self-supporting flywheel and Japan demonstrates what having a mediocre mix of sluggish dynamism, risk aversion and feeble, old-demo support structures can do. The immediate policy implications are therefore pragmatic and uncompromising. The pendulum will swing toward those political economies that make experimentation routine rather than exceptional, not only toward those who merely wish it weren't the case. It is still possible; the outstanding scientific and industrial endowments do remain, along with the large consumer markets. An ever-more-fragmented support architecture, an absent early-stage high-pressure system and the weak elective incumbency will result in a new generation of European a digital "follower," not a pioneer of its own.

5. Conclusion - The Adoption Gap Is an Institutional Gap

The AI adoption divide is not a narrow story about enthusiasm, regulation or access to digital tools. It reflects a deeper institutional separation between economies that combine elite technical talent, risk-tolerant capital and active state support and economies that possess these assets only in partial or fragmented form. The United States leads because its firms, universities, investors and public institutions convert AI from an available technology into an organizational capability. China remains a credible challenger because it has built a more centralized version of the same triad. Europe and Japan, despite their technological sophistication, show how weak investment incentives, cautious management, uneven skill pipelines and protected incumbency can slow adoption even where awareness is high.

The policy implication is therefore structural. AI will not simply raise productivity wherever it appears; it will widen the gap between firms, regions and workers that learn quickly and those allowed to postpone change. Europe still has scientific depth, industrial assets and consumer scale, but these advantages will matter only if they are joined to capital formation, managerial renewal, stronger AI-relevant skills and sharper competitive pressure. AI leadership will belong to political economies that make experimentation routine, organizational learning unavoidable and institutional adaptation faster than decline.

References

[1, 7] Brookings Institution (2026) Why Is the U.S. Outpacing European Countries in AI Adoption? Brookings Institution.

[2, 3, 6, 15] Bick, A., Blandin, A., Deming, D., Fuchs-Schündeln, N. and Jessen, J. (2026) Mind the Gap: AI Adoption in Europe and the U.S. Federal Reserve Bank of St. Louis.

[4] Eurostat (2026) Use of Artificial Intelligence in Enterprises. European Commission / Eurostat.

[5] CEPR / VoxEU (2026) Differences in AI Adoption in Europe and the US: Explanations and Implications for Productivity Growth. Centre for Economic Policy Research.

[8] Brynjolfsson, E., Li, D. and Raymond, L. (2023) Generative AI at Work. National Bureau of Economic Research.

[9, 45] Bank for International Settlements (2026) AI Adoption, Productivity and Employment: Evidence from European Firms. BIS Working Papers.

[10, 11, 16] Stanford Institute for Human-Centered Artificial Intelligence (2025) AI Index Report 2025. Stanford University.

[12] Reuters (2025) China to Set Up National Venture Capital Guidance Fund, State Planner Says. Reuters.

[13, 14, 20, 41] European Investment Bank (2025) European Investment Bank Investment Survey 2025. European Investment Bank.

[17, 18, 39, 40, 47] Draghi, M. (2024) The Future of European Competitiveness. European Commission.

[19, 40] International Monetary Fund (2025) Europe’s Productivity Weakness: Firm-Level Roots and Remedies. International Monetary Fund.

[21] Eurostat (2025) Individuals’ Level of Digital Skills. European Commission / Eurostat.

[22] Eurostat (2026) ICT Specialists in Employment. European Commission / Eurostat.

[23] European Commission (2025) Union of Skills. European Commission.

[24, 26] European Commission (2025) AI Continent Action Plan. European Commission.

[25] OECD (2025) Progress in Implementing the European Union Coordinated Plan on Artificial Intelligence. OECD Publishing.

[27] National Artificial Intelligence Initiative Office (2025) National AI Research Institutes. NAIIO; National Science Foundation (2025) NSF Invests $100 Million in New National AI Research Institutes. NSF; White House (2025) America’s AI Action Plan. Executive Office of the President.

[28, 29, 46] OECD (2025) Emerging Divides in the Transition to Artificial Intelligence. OECD Publishing.

[30] OECD (2025) The Digital Transformation of SMEs. OECD Publishing; Reuters (2024) More Than 40% of Japanese Companies Have No Plan to Make Use of AI. Reuters.

[31, 32, 43] OECD (2024) OECD Economic Surveys: Japan 2024. OECD Publishing.

[33] OECD (2025) Education at a Glance 2025: OECD Indicators. OECD Publishing.

[34] OECD (2026) OECD Economic Surveys: Japan 2026. OECD Publishing; Reuters (2026) Japan Looks to Let More “Zombie” Firms Close or Merge to Restore Economic Metabolism. Reuters.

[35] Ministry of Economy, Trade and Industry of Japan (2025) GENIAC: Generative AI Accelerator Challenge. METI; Government of Japan (2025) AI Act, AI Basic Plan and AI Strategic Headquarters. Government of Japan.

[36] Digital Agency of Japan (2026) Government AI “GENAI”. Digital Agency, Government of Japan.

[37] National Bureau of Economic Research (2026) Firm Data on AI Adoption. NBER.

[38] European Central Bank (2025) Firm Age, Productivity and Intangible Investment in the Euro Area. European Central Bank.

[42] European Commission (2025) Digital Markets Act Proceedings Against Apple and Meta. European Commission.

[44] Government of Japan (2025) AI Strategy and Business Dynamism Policy Materials. Government of Japan.